Algorithmic Stablecoins: The fragile negative feedback loop

The essence of algo stablecoins' failures is unexpected feedback effects

All the algorithmic stablecoins aim to build reliable and sustainable negative feedback mechanisms. More specifically, the core approaches are arbitrage mechanisms design.

I want to discuss some algo stablecoin instances to emphasize it’s impossible to build algo stablecoins without collaterals. To clarify, collaterals only refer to core crypto assets like BTC and ETH which have very strong consensus and utility.

LUNA/UST

The recent example is LUNA/UST system. I will explain the general process about booming and collapsing of a 40 billion asset. The negative feedback mechanism of LUNA/UST to maintain stable is as following:

When price of UST is lower than 1 USD, arbitragers in the market will buy UST at discount then convert to 1 USD worth of LUNA in Terra Station. Then, arbitragers sell the 1 USD worth of LUNA to get profit.

When price of UST is higher than 1 USD, arbitragers in the market will buy 1 USD worth of LUNA and convert to 1 UST in Terra Station. Then, arbitragers sell the 1 UST at market to get profit.

Seems like a perfect feedback mechanism. However, after scaling and projecting the system with a larger balance sheet, positive feedback loop in negative direction could destroy everything.

In the initial phase of the system, the positive feedback loop will accelerate growth and boost the system to prosperity. In this phase, UST is over-collateralized and the market is confident about both the stability of UST and growth potential of Terra ecosystem. More and more investors come into the system and chase the profits (~20% APY) provided by Anchor protocol. Everyone is happy in this phase and gets addicted to high and fixed yield. This is phase 1 as following picture shows.

However, you can never print money out of thin air and there is limitation of growth. After rapid growth from May 2021, the system reached a critical state of collapse in May 2022.

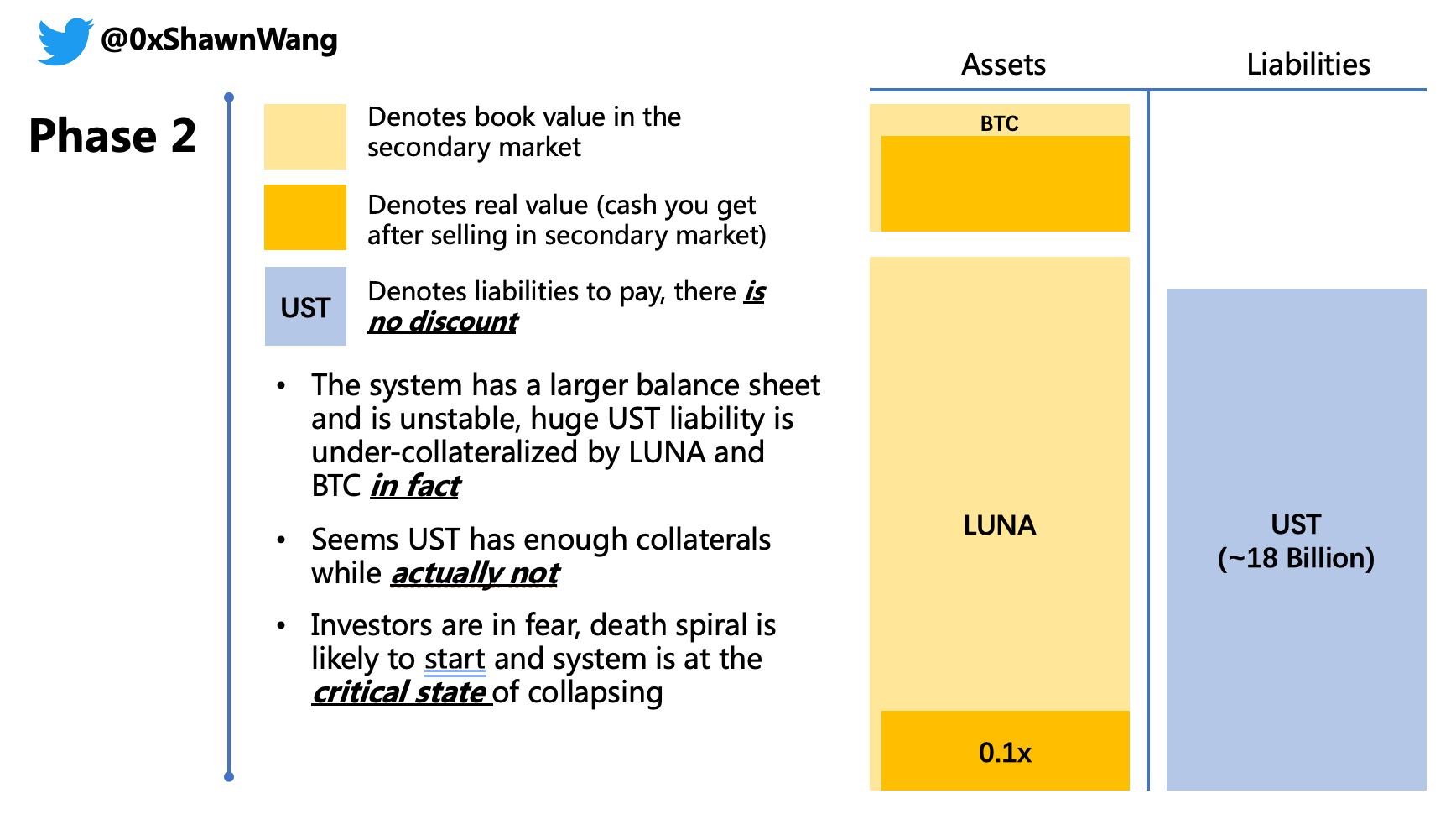

In phrase 2, UST is in danger and under-collateralized and the collateral assets (LUNA and BTC) and could only cover the UST market cap in book value. In fact, even only a relatively small amount of people decide to quit this game by selling their LUNA or UST position, the system will collapse. Or, if macro environment turns down and money supply reduces, the price of LUNA and BTC will drop, which makes UST become under-collateralized. If these two factors add up and resonate, the system will be very fragile which is just the situation Terra encountered.

In the phrase 3, the positive feedback loop appears and destroys the system in a speed faster than everyone’s expectation. Once an increasing number of people find the signs that UST cannot be repaid, they will sell their UST/LUNA position desperately and lead to more severe bank-run and catastrophe.

If we summarize the 3 phases of LUNA's algorithmic stablecoin system briefly. There is an obvious paradox in the whole process: the low-level negative feedback mechanism becomes a tool to generate positive feedback. It’s because arbtragers will buy UST and covert to LUNA than sell in the market.

Stablecoins need stability and equilibrium, which are guaranteed by negative feedback. However, in fact, the system just keeps growing until reaching its peak or limitation and starts collapsing since simple one-way positive feedback always leads to system crashes due to growth limitation.

In addition, the feedback effect transmitted in blockchain is quite fast since all information is transparent and available. Thus, in extreme condition panic will spread rapidly since everyone know the true and terrible situation. Also, smart contract works all the time and lots of steps and procedures are automated. Such features only increase instability in a market filled with human irrationality and reflexivity.

Let's walk through other examples in the algorithmic stablecoins field.

Ampleforth

Ampleforth employs the rebase mechanism: the ideal negative feedback loop mechanism is directly changing the token amount of all token holders. When the price of AMPL is over 1 USD, the balance of all AMPL addresses will increase in proportion, which assumes more supply will press the price back to 1 USD. Conversely, when the price is under 1 USD, the balance of all AMPL addresses will decrease in proportion, which assumes less supply will push the price to 1 USD.

However, unexpected positive feedback loops appear. When the price of AMPL is higher than 1 USD, holders are more willing to hold instead of to sell since holding AMPL holders get more inflation supply of the protocol and own more AMPL tokens. Such action decreases token supply and pump the price. Then, the protocol continues to allocate more inflation rewards to AMPL holders and token supply in the market reduce further. Correspondingly, a positive feedback loop in opposite direction when the price of AMPL is under 1 USD.

Basis Cash

The basic idea of Basis Cash is to absorb instability and fluctuation of the BAC (stablecoin) by creating equity token BAS (Basis Shares) and bond token BAB (Basis bonds).

Basis Cash's ideal negative feedback mechanism is as following:

When price of BAC is higher than 1 USD, the protocol will mint new BAC to BAS holders to increase supply and try to press the price back to 1 USD. The protocol assumes holders will sell BAC in the open market to expand circulation supply of BAC.

When price of BAC is under 1 USD, the protocol will trade BAB for BAC in the market to reduce supply and push the price back to 1 USD. Next time when the price of BAC is above 1 USD, the newly minted BAC will be allocated to BAB holders in priority and BAB will be burned. After all existing BAB is burned, the rest of newly minted BAC will be allocated to BAS holders.

However, the unexpected positive feedback loop reverses and disturbs the system. The expected scenario is BAS holders will sell their BAC and increase supply in market to lower the price. But the real case is BAS holders tend to hold the newly minted BAC to get more and the price of BAC continues to above 1 USD. If more people hold their BAC, the circulation of BAC reduces and price become higher.

In the opposite direction, people are less willing to maintain peg of BAC when the price is lower than 1 USD, since the people trade BAC for BAB need to convince themself the price of BAC could be higher than 1 USD in future. However, the lower the price, the smaller the probability of price could go above of 1 USD. It’s a positive feedback loop in opposite direction.

Iron Finance

Iron Finance's ideal negative feedback mechanism is as following:

Arbitrageurs were expected to stabilize the price of IRON because there was an incentive.

If price goes down, they can buy cheap IRON from the market, redeem it for USDC+TITAN (1 IRON produces 1 USD worth of USDC+TITAN when redeeming) and sell TITAN for some profit. Such buying from the market would eventually rise the price of IRON.

If price goes up, they will mint new IRON (1 IRON requires 1 USD worth of USDC+TITAN when minting) and sell them on the market to get the difference as a profit. Selling would eventually drop the price of IRON.

However, the unexpected positive feedback destroys the system and the price of TITAN (governance token of Iron Finance) crashes and goes to zero. It's because the oracle of the protocol employs TWAP (time weighted average price). When price of TITAN continues to drop, the real-time price on the market is lower than the oracle price, which means there are no profits for arbitragers and IRON continue to depeg.

The depeg of IRON further spreads the fear which leads to people selling TITAN and IRON directly in the market. As the selling by whales further decreased the price of IRON, more TITAN was constantly minted and press the price to zero. Huge amount of TITAN increases the supply and destroys the system just like LUNA/UST system. The lower the market cap of TITAN, the lower the people’s confidence on IRON will be and continue to sell IRON and accelerates depeg process.

Summary

Stability is core and necessary of a stablecoin. However, crypto market is extremely volatile and reflexive that makes it very difficult to build a reliable negative feedback loop. In the above analysis, we find various positive feedback loops come into place and disturb the equilibrium.

The original intention of stablecoins is to become hard currency to hold in extreme market condition just like USD. However, the reality is negative feedback loop of pure algo stablecoins without collaterals become very fragile and risky in crisis or extreme situation. This is an inherent problem without solution. A simple analogy is a system without constant energy interaction with outside cannot be vibrant and prosperous and pure algo stablecoin is this case. If some brand-new ideas emerge and possibly work out the problem, it should be completely different from the existing artificial designs.